Will They Return?

One-Sixty is so Close, you can almost touch it But, will they return?

The current Mr Yen, Masato Kanda, was on the tape last night as USDJPY creeps ever closer to the 160 level that triggered the most recent bout of inflation at the end of April. He explained, “If there are excessive currency fluctuations, it has a negative impact on the national economy. In the event of excessive moves based on speculation, we are prepared to take appropriate action.” At this point, the overnight high of 159.89 is just 28 pips from the peak seen prior to the last bout of intervention, although the price action this time is far more muted than what we saw then. While the yen’s decline has been steady, as can be seen in the below chart, it hasn’t been so swift it appears out of control.

Source: tradingeconomics.com

One of the key rationales for the previous bout of intervention was that the weakening of the yen occurred too rapidly, with a 10-yen decline seen over a short six-week period. That has not been the case this time, so I do not anticipate any MOF/BOJ action at 160, but rather somewhere closer to 165 if we see that during the summer. Remember, the BOJ meets again at the end of July at which point they are expected to present their new bond buying program with reduced amounts of JGBs, their version of QT. Remember, too, that there is still a huge interest rate differential between the US and Japan, and until that narrows, and is expected to narrow further, it is very difficult to see the yen showing any substantive strength. While caution is merited here, as the BOJ can certainly enter the market at any time, based on the summary of opinions from the last BOJ meeting, which were released last night, there is no clear consensus on the pace of either QT or rate hikes. The yen seems to have further to fall this summer.

In China, the powers that be Are scared that their own renminbi May fall and expose The emperor’s clothes Are missing, and that all might see

As things in the West are awaiting two key events at the end of the week, the PCE data in the US on Friday and the French elections on Sunday, we shall continue our look at Asia. The CNY market onshore is frozen as it is pegged at the 2% maximum movement from the daily CFETS fixing. Last night’s fixing of 7.1201 indicates that the highest the dollar can trade on shore is 7.2625, the level at which it is currently pegged. In fact, given the interest rate differentials between the US and China, funding of traders’ books is becoming impossible because the one-day forward points will result in a price above the band.

While the offshore renminbi is slowly grinding lower, the pressure on the PBOC to adjust its daily fixing more rapidly grows. This issue is a result of the following incompatible goals as defined by President Xi; support the collapsing local property markets by easing monetary policy while maintaining a stable and strong renminbi to demonstrate to the world that CNY should be a global currency (despite the capital controls in place!). Alas for President Xi, these two ideas do not work in concert with the result that onshore FX markets are likely to remain frozen until things change. A look at President Xi’s history tells me, at least, that like the Red Queen, he can believe multiple impossible things at the same time. Ultimately, the great irony here is that despite Xi’s desires to demonstrate the importance of the renminbi to the world, he is entirely reliant on the Fed to cut rates in order to break this deadlock, and I strongly suspect that Chairman Powell cares not one whit about Xi Jinping and his problems.

Looking ahead, I anticipate the renminbi will grind lower over time as it remains the only outlet for the still lackluster growth in the economy with the property market problems forcing interest rates lower than otherwise would be desired. Arguably, this is why the Chinese, in their current bout of trade talks with the EU, is demanding that Europe removes its tariffs on Chinese EVs. Since they can’t weaken the currency further, they need to get the other side to effectively cut prices for them.

Ok, let’s review the overnight activity. After Friday’s lackluster equity markets in the US (the NASDAQ actually fell, which I thought was illegal), the picture in Asia was mixed with the Nikkei (+0.5%) rallying a bit as the weak yen continues to support their exporters, while mainland Chinese shares (-0.5%) suffered as the ongoing weak economic data (Friday night showed Foreign direct investment fell -28.2% YTD, the weakest performance since 2009, and another indication that the renminbi is too strong). As to the rest of the region, there were more laggards (Korea, Taiwan, Australia, New Zealand), than gainers (India, Singapore, Thailand). However, in Europe this morning, the screens are all green as the limited data, German Ifo, indicated continued weakness raising hopes for a July rate cut by the ECB. As to the US futures market, at this hour (7:15), they have edged slightly higher, about 0.15%.

Treasury yields have moved higher by 1bp but remain far closer to recent lows than the highs seen a month ago. But the story in Europe is interesting as the Bund-OAT spread has narrowed by 5bps after comments by the RN party’s Jordan Bardella, the leading candidate as new PM, that were far more muted and accepting of Europe as a whole, and less populist financial goals. This has played itself out across the entire continent with the perceived weaker countries seeing their yields slide slightly while Germany and the Netherlands have seen yields edge higher. In Asia, JGB yields backed up 2bps to 0.98%, arguably in response to the summary statements from the BOJ.

Oil prices are continuing to show strength, up another 0.5% this morning, as the inventory draw from last week continues to support the market. Meanwhile, after a very difficult session on Friday, metals prices are stabilizing with gold and silver both up 0.15%, although copper, which was higher earlier in the session, has now reversed course and is down -0.6%.

Lastly, the dollar is broadly, though not universally, under pressure this morning, with the euro (+0.35%) the driver in the G10 market which is also dragging the CE4 higher (PLN +0.9%, HUF +0.5%). Bucking the trend is the rand (-1.0%) as market participants start to wonder who President Ramaphosa will be appointing to his cabinet now that he must share power. One must be impressed with the volatility in the rand of late, that is for sure.

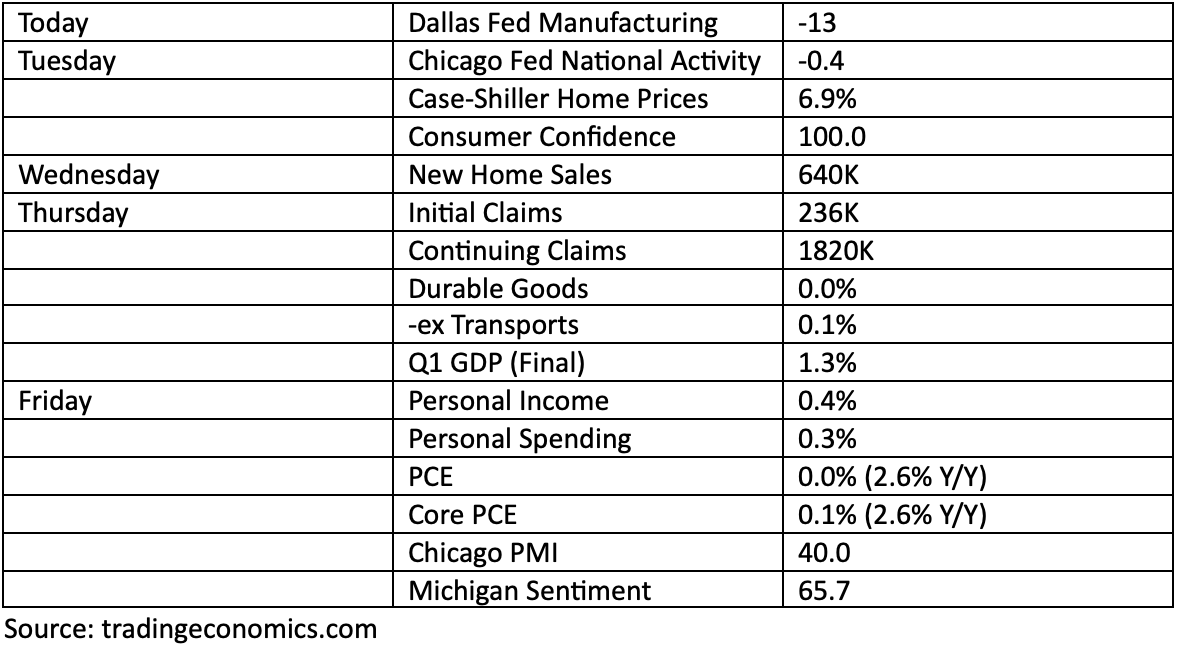

On the data front, while we get several indicators earlier in the week, all eyes will be on Friday’s PCE data.

As well as the data, we hear from five more Fed speakers with Governor Michelle Bowman speaking at three separate events this week. However, thus far, there has been no substantive change from the Powell mantra that they need to see more evidence that inflation is slowing, several months’ worth, before considering easing policy. Of course, if next week’s Unemployment rate were to tick up to 4.2%, I imagine that mantra might change.

On the central bank front, only Sweden’s Riksbank meets this week, and no policy change is expected. If you recall last week, the bulk of the data was soft in the US, although the PMI data surprised to the high side. However, if the data set is beginning to show more weakness, I suspect the Fed will begin to hint that cuts are possible sooner, rather than later. Right now, the market is pricing about a 10% probability for the July meeting, but more than a two-thirds probability for September. A little more weak data and I will likely adjust my views of rate cuts coming. At that point, I think the dollar will suffer significantly. But until we get a lot more evidence that is on the way, I think the default is the dollar is still the best bet.

Good luck

Adf